{kind=link}

Table of Contents

The Move Towards a Cashless Society in Australia: An Analysis

Despite claims of increasing cash circulation in Australia, the nation’s economy is rapidly transitioning toward a cashless society. As digital payment methods rise in popularity, cash transactions are declining sharply.

Disputes Over Cash Usage Statistics

The Australian Banking Association (ABA) CEO, Anna Bligh, recently stated that physical cash usage has plummeted from 70 per cent of transactions in 2007 to about 10 per cent today. She referenced projections from the Reserve Bank of Australia (RBA) estimating that this figure could drop to around 4 per cent by 2030. Contrarily, the cash advocacy group Cash Welcome challenged these assertions, accusing Bligh of perpetuating myths about Australia’s cash usage. They pointed out that current RBA statistics indicate that cash is still involved in 16 per cent of in-person transactions.

The Paradox of Cash Circulation

Interestingly, while fewer transactions utilise cash, the overall amount of cash physically circulating in Australia has never been higher. An RBA report from 2021 noted that the rise in banknotes can be attributed to people saving cash rather than spending it. Indeed, around 73 per cent of all banknotes by number, and a staggering 94 per cent by value, are in $50 and $100 denominations, further emphasising this trend towards saving.

When adjusting for population growth, the per capita cash in circulation has decreased from a peak of $3,987 in 2021 to $3,750 currently. Despite claims of increasing cash availability, the argument doesn’t translate into higher daily usage.

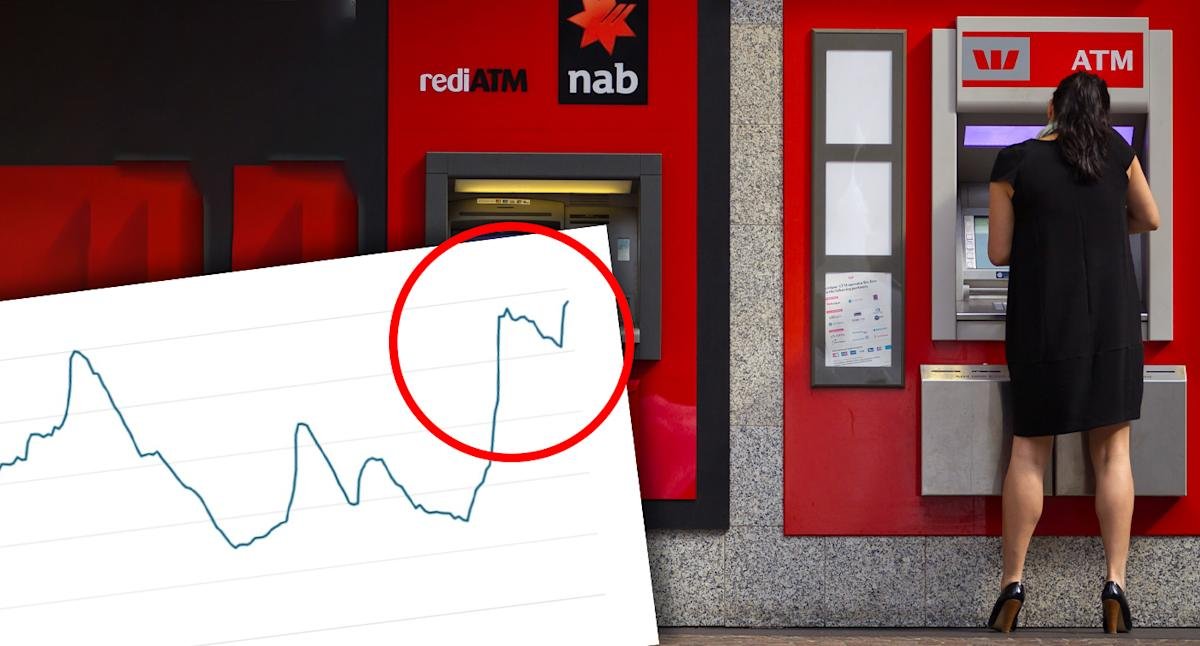

Declining ATM Withdrawals

Further analysing recent data reveals a troubling trend. The volume of cash withdrawals from ATMs has been declining significantly since 2009, with current monthly withdrawals hovering around 28 million, compared to 75 million at their peak. While there was a minor uptick following COVID lockdowns, the numbers remain below previous averages.

Social Implications of a Cashless Transition

The push for a cashless society raises pertinent social questions. Individuals in vulnerable positions, such as those experiencing homelessness, often rely on cash donations. Some vendors have adapted by accepting card payments, but the lack of cash options can exacerbate inequalities.

The RBA’s latest Consumer Payments Survey noted cash transactions fell from 69 per cent in 2007 to just 13 per cent in 2022, with cash accounting for only 8 per cent of all payment values. This demonstrates that Australians overwhelmingly favour digital payment methods, with cashless transactions now the norm.

Financial Considerations for Businesses and Consumers

While cash transactions have their benefits, such as anonymity and perceived security, digital payments involve their own set of fees. Merchants face expenses associated with handling and securing cash, and many are beginning to pass on card surcharges directly to consumers. Addressing these card surcharges, alongside managing the costs of cash, will be crucial as Australia continues its transition toward a digital economy.

Regulation mandating businesses to accept cash could be considered regressive; instead, a more balanced approach might be found in the UK’s prohibition on surcharges for any payment type. According to Finder’s Consumer Sentiment Tracker, over 50 per cent of Australians do not carry cash at all. This indicates a significant shift in consumer behaviour, and it appears unlikely that Australians will revert to carrying cash in the future.

Conclusion: A Cashless Future

The data clearly illustrates that Australia is on the verge of becoming a predominantly cashless society. While there are logistical and social challenges associated with this shift, the reality is that cash transactions are becoming increasingly rare. Consumers and businesses alike are adapting to a landscape where digital payments dominate, leaving cash as a less utilised method of transaction.