{kind=link}

The Rise of Cashless Transactions in Australia: A Closer Look

Australia is witnessing a profound transformation in its payment landscape, marked by a significant decline in cash transactions. Despite claims from some groups that cash is part of everyday life, a closer examination reveals a rapidly evolving cashless society.

The Current State of Cash Usage

Debates about cash usage have intensified, particularly with comments from Anna Bligh, CEO of the Australian Banking Association (ABA), who stated that cash transactions have plummeted from 70% in 2007 to approximately 10% as of now—projected to drop to 4% by 2030 according to the Reserve Bank of Australia (RBA). However, advocacy group Cash Welcome has countered these figures, citing RBA data that suggests cash still accounts for about 16% of in-person transactions.

Cash Welcome argues that the banking industry is perpetuating a myth about declining cash use. This has sparked a dialogue about the actual figures and the implications of this shift towards digital payments.

Understanding the Numbers

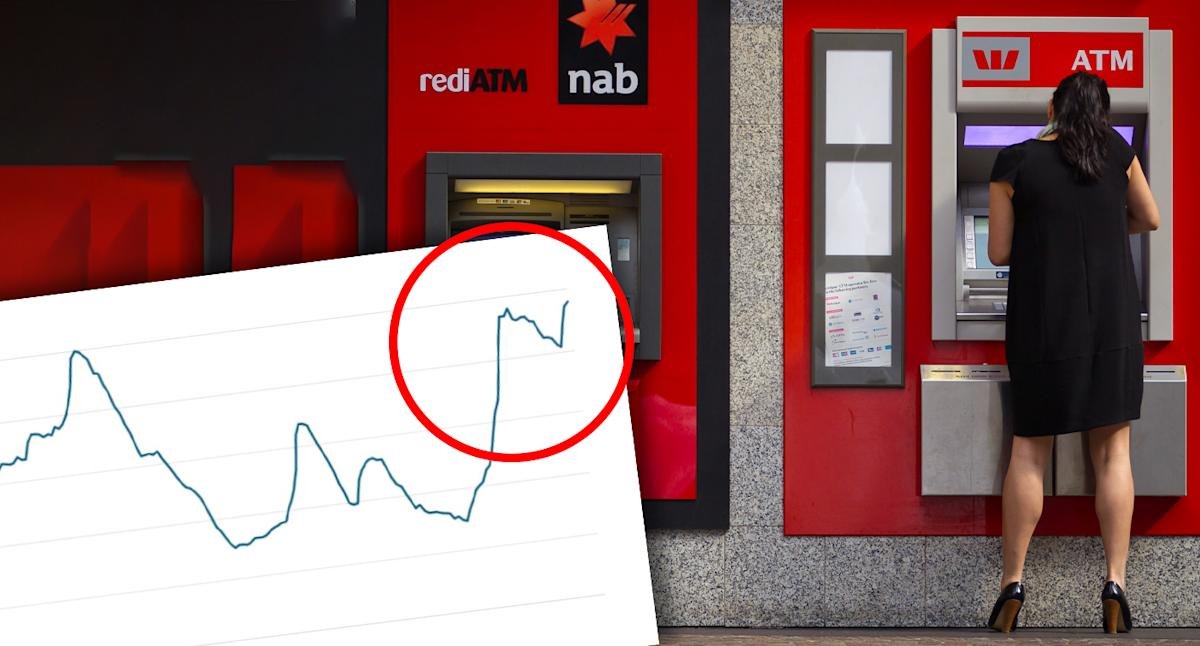

While the RBA’s projection indicates a significant fall in cash transaction volumes, data shows a curious contradiction: even as cash payments decrease, the amount of physical cash in circulation has reached all-time highs. This increase can be attributed to a shift in consumer behaviour, where cash is often saved or stored rather than utilised for purchases. It’s noteworthy that a staggering 73% of physical banknotes in circulation are in higher denominations like $50 and $100, suggesting they are primarily viewed as a vehicle for wealth storage.

Adjustments for Australia’s population growth reveal that cash per capita is declining. From a peak of $3,987 in 2021, the figure fell to $3,750 by March 2025. This reflects a broader trend away from cash usage, underscoring the limited relevance of increased total cash in a growing population context.

Diminishing Withdrawals

Despite claims that ATM and over-the-counter withdrawals remain stable, data indicates a dramatic decline in ATM usage, dropping from around 75 million monthly withdrawals in 2009 to approximately 28 million today. This trend has remained consistent even after temporary increases following COVID-19 lockdowns.

The move towards cashless transactions isn’t simply a statistical anomaly; it has tangible consequences. The RBA’s latest Consumer Payments Survey shows that cash transactions plummeted to 13% of all payments in 2022, with cash accounting for merely 8% of total transaction value.

The Human Cost of Going Cashless

While the convenience and efficiency of digital payments are apparent, the transition to a cashless society could have negative implications for certain demographics. The homeless, for instance, often depend on cash donations, highlighting a social cost to the declining use of physical money.

However, adaptations are emerging; many vendors, such as those from the Big Issue, are experimenting with digital payment options to meet changing consumer preferences.

Balancing Costs and Accessibility

As cash transactions decrease, the costs associated with transporting and managing cash are rising. ABA has noted that the dwindling use of cash increases the financial burden of cash distribution. Furthermore, cash-only businesses may escape some tax obligations, thereby impacting government revenues that fund crucial services.

While card payments can attract additional fees, the costs associated with cash management are equally significant. Businesses incur expenses related to cash handling that are growing, necessitating a reevaluation of how payments are processed.

Navigating the Transition

There’s a rising consensus that businesses should have the discretion to choose cash or digital transactions without being forced into either framework. Striking a balance between promoting cashless payments while ensuring access—similar to the UK’s prohibition on surcharges for any payment type—could be a prudent strategy moving forward.

Finder’s Consumer Sentiment Tracker reveals a noteworthy trend: over 50% of Australians report not carrying physical cash at all. As digital transactions become the norm, it appears that a return to cash-dominant practices is highly improbable.

In conclusion, Australia is on a pronounced trajectory towards a cashless economy. The associated benefits of efficiency and reduced costs come with challenges—especially for vulnerable populations that depend on cash. The discourse surrounding cash’s future in Australia underscores a critical transition in consumer payment preferences, revealing that the future may indeed be digital.