{kind=link}

Table of Contents

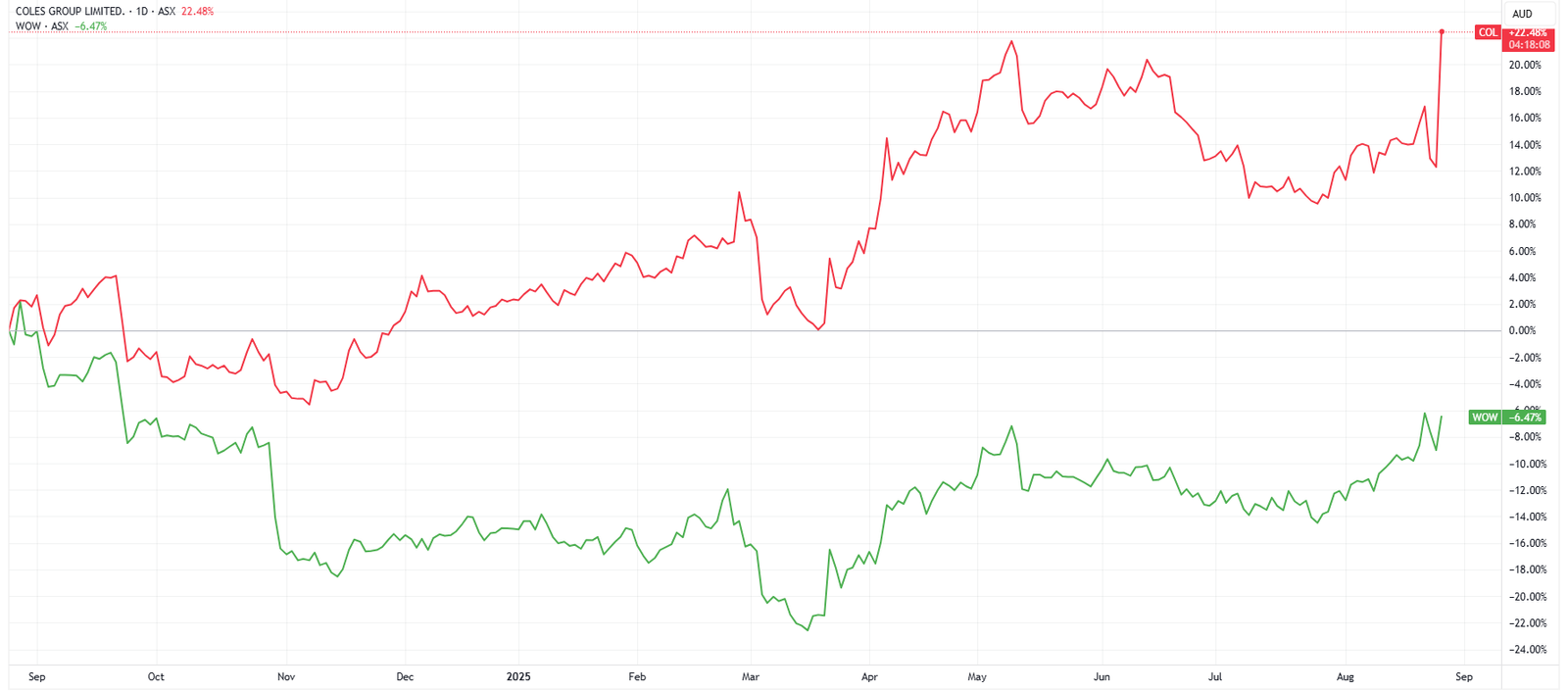

Investors have shown a strong interest in Coles Group (ASX: COL) following the release of its solid financial results for FY25, which met or surpassed many analyst targets. On Tuesday, shares opened 3.5% higher and have climbed 9.2% to $22.64.

FY25 Financial Summary

Coles’ earnings growth was supported by significant operational efficiencies and an upturn in supermarket sales, even though its liquor division underperformed.

- Revenue: Increased by 3.6% to $44.35 billion, in line with expectations.

- Underlying EBITDA: Rose 11% to $4.05 billion, exceeding estimates by 2.3%.

- Underlying EBIT: Up by 7.5% to $2.22 billion, outperforming forecasts by 5.7%.

- Underlying NPAT: Reached $1.18 billion, surpassing estimates by 6.3%.

- Total Dividend: Proposed at 69 cents per share, higher than Goldman Sachs’ expectations of 64 cents, reflecting a 7.8% upside.

Operational Highlights

This year has seen significant operational milestones for Coles, such as:

- Enhanced customer experience metrics across availability, quality, range, and checkout efficiency.

- Successfully managed a 30% drop in tobacco sales, now constituting less than 3% of total revenue, down from a high of 8% in FY19.

- Introduced 970 new products at key trade events throughout the year.

- eCommerce sales surged 24.4% to reach $4.5 billion, increasing online sales penetration to 11.2%.

- Opened two automated Customer Fulfilment Centres (CFCs) in early FY25.

- Renewed 60 stores, launched eight new locations, and closed four, bringing the total to 860 supermarkets.

Another positive point is the FY26 trading update, with sales in the first eight weeks rising by 4.9% year-on-year, outpacing the consensus prediction of 3.6% growth.

Analyst Insights

Analysts from Jarden provided a positive evaluation, stating, “It’s a solid, straightforward result where the one-off costs associated with supply chains are accounted for. The tone of the release feels optimistic, pointing to a robust start in FY26 and reinforcing belief in operational leverage beginning to manifest in the profit and loss statement.”

They indicated that this strong performance may lead to upward revisions in target prices, though a Neutral rating may persist due to current valuations. Goldman Sachs, earlier this month, remarked that “Coles is trading at approximately 23 times its one-year forward price-to-earnings ratio, with an expected EPS growth of around 11% from FY25 to FY27 compared to its long-term average of 21.3 times.”

Coles vs. Woolworths

Coles has shown notable strength compared to Woolworths, outperforming it with a 22% return over the past year.

The crucial question moving forward is whether Coles’ results reflect its own improved performance or if Woolworths has faced challenges. Jarden analysts have referenced previous discussions indicating that Woolworths was believed to be performing better.

In summary, Coles’ FY25 results underscore a strong financial position, benefiting from strategic efficiencies and growth in core areas, despite a challenging liquor market. The potential for future stock upgrades exists, tempered by caution around valuation metrics. As the company continues its expansion, the comparison with Woolworths will be critical to watch in the coming periods.