{kind=link}

Table of Contents

Iron Ore Prices Expected to Decline Amid Surging Supply and Weakening Demand

According to UBS, iron ore prices are set to decline in the next 12 months as the global market transitions from balance to surplus. Currently averaging around US$100 per ton, the forecast predicts a drop to US$90, driven by increased supply outpacing demand.

Anticipated Supply Surge

A significant rise in iron ore supply is expected through 2027, particularly from Australia and Brazil, which are projected to increase production by approximately 3% annually in 2026 and 2027, adding about 120 million tons.

Key projects include Fortescue’s Iron Bridge facility, contributing 22 million tons per annum, and Mineral Resources’ Onslow Iron project, which will add 35 million tons. The Simandou project in Guinea is set to revolutionise supply, slated to export 120 million tons by late 2025, dramatically altering global supply dynamics, as highlighted by UBS analysts.

Declining Demand from China

As supply rises, demand faces challenges, especially from China, the world’s largest consumer of iron ore. China’s steel consumption is projected to decline by 1% annually over the next three to five years due to a contraction in the property and construction sectors and ongoing trade disputes that are hindering manufacturing activities.

Signs of moderation in steel production were evident in May and June, with utilisation rates dropping despite robust export levels of around 120 million tons in May.

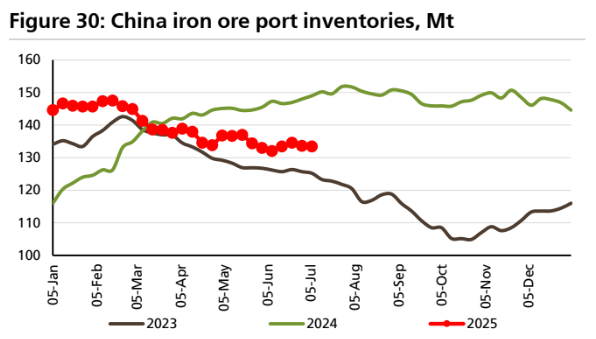

Signs of Market Softening

Several indicators suggest that the iron ore market is cooling:

- Rising iron ore inventories at Chinese ports and mills.

- Recovery of seaborne shipments from traditional suppliers post-disruptions.

- Low steel trader inventories contrasted with increasing port stockpiles.

- Negative speculative positioning on China’s Dalian exchange.

Source: UBS

Price Outlook and Cost Considerations

UBS analysts believe that iron ore prices will find support in the range of US$80-100, aligning with the 90th percentile of the global cost curve. At this price point, some domestic production in China, along with operations in India and smaller Australian and Brazilian mines, may become unprofitable.

Should prices dip below US$90, major miners—Rio Tinto, Vale, BHP, and Fortescue—might halt expansion projects, shifting their focus from volume to value in their strategies.

Long-term Market Structural Changes

Beyond 2027, the iron ore market will encounter further challenges. China’s emissions trading system is tightening, potentially leading to an increase in the use of recycled steel scrap as a substitute for iron ore. While the timeline and impact of this transition are uncertain, it represents an additional structural headwind for demand.

There could be a potential increase in iron ore demand from India and Southeast Asia, where rising wealth levels are often linked to higher steel consumption; however, this growth is unlikely to fully compensate for the decrease in demand from China.

Market Implications

With a cautious market outlook, UBS maintains Neutral ratings on steel producers such as Vale, Rio Tinto, BHP, and Fortescue. Current spot prices of around US$94 already seem to be factoring in anticipated surplus conditions for the latter half of 2025, indicating that the market is aware of the significant shift approaching.

In summary, the iron ore market is poised for evolving dynamics as supply increases while demand, particularly from China, shows signs of decline. Investors and stakeholders should be prepared for a landscape characterised by shifting balances of power, costs, and long-term structural changes.