{kind=link}

Table of Contents

Australian Data Centre Stocks: A Valuation Opportunity Amid AI Growth

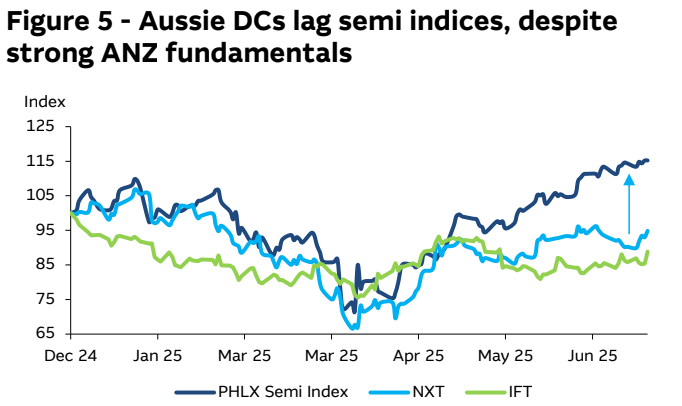

Several Australian data centre stocks, notably NextDC (ASX: NXT) and Infratil (ASX: IFT), are currently trading significantly lower than the Philadelphia Semiconductor Index, a crucial indicator for artificial intelligence (AI) investments that tracks the 30 largest semiconductor firms in the United States. Analysts at Macquarie believe that this disparity presents an appealing value opportunity as global investment in AI infrastructure accelerates.

Valuation Discrepancy

Since reaching lows in March, NextDC has lagged behind the Philadelphia Semiconductor Index by 22%, while Infratil has underperformed by 18%. This disconnect is particularly surprising given the historically tight correlation between Australian data centre stocks and the performance of global semiconductor companies.

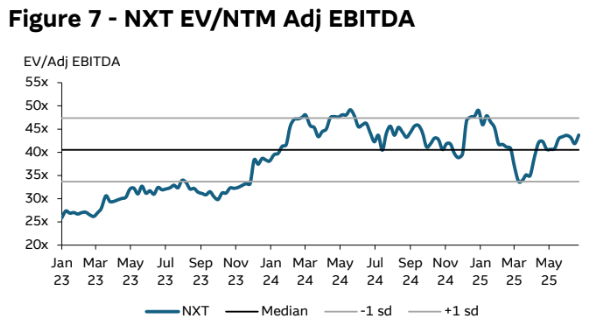

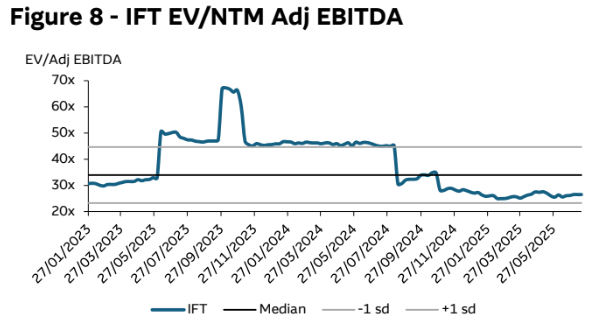

Both NextDC and Infratil are trading below one standard deviation of their median multiples during the ongoing AI era. This situation indicates that their current valuations might not accurately reflect their inherent value.

Source: Macquarie Research, July 2025

Source: Macquarie Research, July 2025

Source: Macquarie Research, July 2025

Strong Demand Fundamentals

The demand for data centres in Australia remains robust, significantly driven by investments from hyperscalers. For instance, Amazon Web Services has recently increased its commitment, resulting in an anticipated demand for 1.8 gigawatts of data centre capacity in Australia. This ongoing demand creates significant growth prospects for both NextDC and Infratil.

If the current contracted and optioned capacity is fully deployed, it could double the earnings for both companies within the next two years. Additionally, other tech giants like Google and Oracle are ramping up their leasing activities in Australia, further underscoring the strong demand environment.

Semiconductor Recovery

The recent rally in the semiconductor sector has been largely propelled by NVIDIA resuming its sales in China, following the easing of US export restrictions related to specialised AI chips. Although NVIDIA suffered from US$2.6 billion in revenue loss and a US$4.5 billion inventory write-off, it still managed to generate US$4.6 billion from chip sales to China in the first quarter.

Speculation suggests that the relaxation of these export restrictions may be part of a wider agreement between the US and China concerning rare earths, thereby restoring confidence in AI infrastructure investments worldwide.

In Australia, an evolving regulatory framework is also diminishing risks associated with supplying enhanced data centre capacity. This, combined with a solid foundation of demand, fosters a favourable environment for expansion.

Conclusion

Macquarie analysts assert that the sell-off in the semiconductor sector back in March wrongly accounted for an AI earnings bubble. However, recent results from major hyperscalers reaffirm the ongoing commitment to global AI infrastructure investment. Australian data centre operators, therefore, appear to be strategically positioned to leverage this emerging trend while still trading at comparatively attractive valuations.

The discrepancy in valuations, relative to historical norms, alongside a recovering semiconductor market, suggests room for multiple expansions in the sector. Given the strong demand drivers and a more favourable regulatory environment, investors may find an enticing opportunity in Australian data centre stocks.