{kind=link}

Table of Contents

Zip’s Shares Surge After Impressive FY25 Results and Encouraging FY26 Outlook

Zip Co Ltd (ASX: ZIP) has made headlines, with its shares witnessing a significant increase of up to 25% in early trading after the company announced impressive results for FY25. The strong performance indicates that Zip is not only solidifying its position in the competitive Australian market but is also experiencing rapid growth in its US operations.

FY25 Highlights

The financial and operational outcomes for FY25 have surpassed consensus expectations in several key areas:

- Total Transaction Value (TTV) rose by 30.3% to AU$13.0 billion, aligning with forecasts.

- Revenue increased by 23.5% to AU$1.08 billion, exceeding expectations by 0.7%.

- EBITDA saw a dramatic rise of 116% to AU$170.3 million, beating forecasts by 6.4%.

- Net Profit After Tax (NPAT) soared by 1,110% to AU$79.9 million, exceeding estimates by 11.3%.

- Earnings Per Share (EPS) was up 785.7% to 6.2 cents, slightly missing forecasts by 7.5%.

A regional analysis reveals that while the Australian and New Zealand (ANZ) market remains steady, Zip’s performance in the US is remarkably dynamic:

- Revenue: US up 46% vs. ANZ down 0.9%

- Total Transaction Volumes: US up 43.9% vs. ANZ up 5.5%

- Transactions: US increased by 33.6% vs. ANZ up 12.6%

- Active Customers: US growth of 11% vs. ANZ up 6.8%

The strong results have underscored Zip’s capability to outperform market expectations, prompting today’s share rally.

Optimistic FY26 Projections

Looking ahead to FY26, Zip’s outlook exceeds expectations, particularly regarding growth in the US:

- US TTV Growth is projected to exceed 35% (in USD), indicating a balance between profitability and growth.

- The Group Revenue Margin is expected to be approximately 8%.

- The Group Cash Net Transaction Margin has been upgraded to between 3.8% and 4.2%.

- The Group Operating Margin is also uplifted to a range of 16.0% to 19.0%.

- The Group Cash EBITDA as a percentage of TTV is anticipated to be over 1.3%.

These forward-looking metrics significantly surpass UBS’s previous estimate of about 25% US TTV growth, providing further fuel for the stock’s positive trajectory.

Exploring a US Dual Listing

In addition to its promising financials, Zip is contemplating a dual listing on the Nasdaq. This move is driven by several factors:

- The US segment is now contributing over 80% of Zip’s divisional cash earnings.

- There is a notable increase in interest from US investors, with offshore institutional investors holding approximately 16% of Zip’s issued capital.

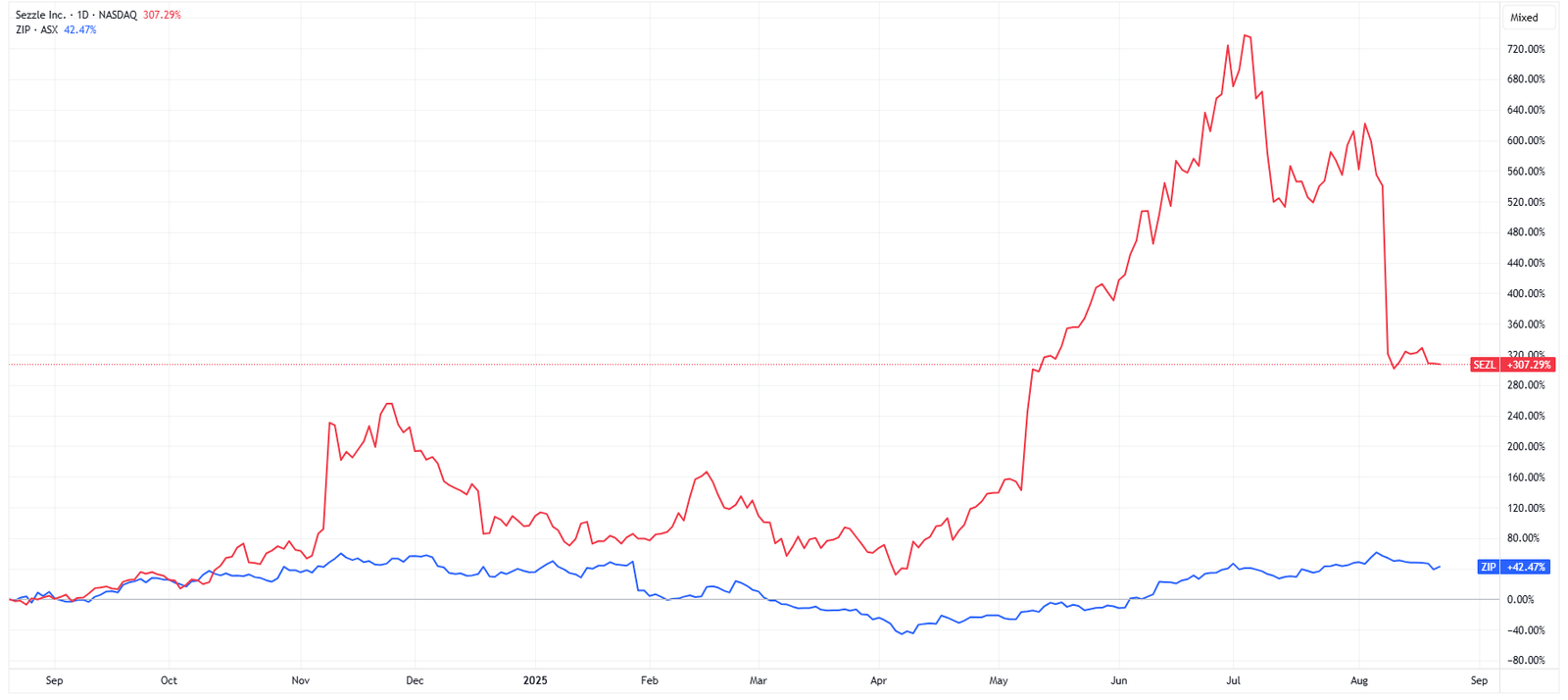

Should this listing come to fruition, it could have a substantial impact on the company’s market position, particularly given Sezzle’s recent success after delisting from the ASX and subsequently experiencing gains on the Nasdaq.

Conclusion

In summary, Zip is on a remarkable upward trajectory, driven by its impressive FY25 results and optimistic FY26 guidance for the US market. This solid performance is expected to attract upgrades from analysts and could lead to increased target prices. However, it is worth noting that the stock has experienced a significant rally of over 200% since touching its lows on Liberation Day, which may raise considerations for investors about the potential for overextension.