{kind=link}

Table of Contents

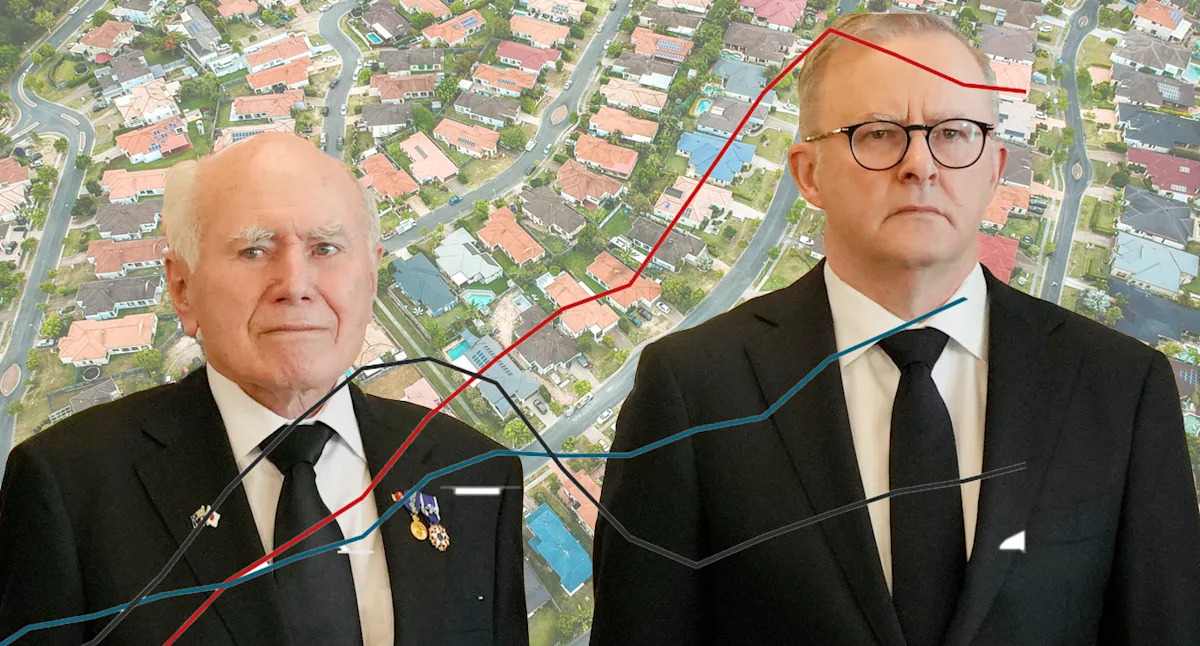

The Evolution of Australia’s Housing Market: From Capital Gains Tax to Affordability Challenges

On 12 May, the Albanese government is poised to unveil a budget which may reshape the economic landscape for decades. Key discussions surrounding this budget focus on potential reforms to the capital gains tax (CGT) discount and negative gearing, vital tools purportedly contributing to intergenerational inequality and the ongoing struggles of many Australians to secure housing.

The narrative behind the CGT discount is complex. Introduced on 21 September 1999 by the Howard government, it allowed taxpayers to exclude 50% of capital gains from their taxable income for assets held over a year. This marked a significant shift away from the previous model of indexation based on inflation-adjusted profits.

At that time, the median house price in Sydney was approximately $272,500, while in Adelaide, it was a mere $127,000. The financial burden for homebuyers was already substantial, with servicing a mortgage on a median Sydney house requiring 37.7% of average full-time earnings. In contrast, other capital cities faced lower mortgage burden levels, well below the 30% threshold indicative of mortgage stress.

The Aftermath of Tax Changes

Following the CGT discount’s introduction, housing prices experienced unprecedented inflation-adjusted growth, marking the most significant increase since records began in 1970. Over the next five years, real housing prices escalated by 50.4%, dwarfing even the dramatic price rises witnessed during the pandemic.

Adding fuel to the housing fire, the Howard government launched a $7,000 cash grant for first-time homebuyers in July 2000, motivated by the impact of the Goods and Services Tax (GST). The grant, which was later increased to $14,000 before the 2001 election, applied to both new and existing homes, resulting in a surge in demand. In markets like Brisbane, this grant represented nearly 8% of the median home price, while in Adelaide, it was close to 10%. Consequently, housing turnover rates skyrocketed, hitting levels unseen since 1990. Despite benefiting many first homebuyers, this instigated long-term price increases, escalating the entry barrier for new buyers.

The federal Productivity Commission observed that assistance targeted towards homebuyers often inadvertently benefited sellers, driving up prices instead of alleviating affordability issues. This irony suggests that while grants aimed to make home ownership more accessible, they instead heightened challenges for those not qualifying for assistance.

Interest Rates and Housing Dynamics

While the CGT discount significantly influenced price growth, it was not the sole factor in play. Between 1995 and 1999, average mortgage rates plummeted from 10.52% to 6.57%, considerably enhancing borrowing capacity. The late 1990s and early 2000s also saw a rise in discounted variable rate mortgages, lowering effective mortgage interest rates further.

In assessing the long-term impact of these dynamics, analysis from the federal Treasury highlights a substantial increase in mortgaged properties held by investors since the CGT discount’s introduction. However, a deeper look into historical trends shows that this increase began in the early 1990s, driven largely by the decline in owner-occupier loans faced with rising interest rates and economic downturns.

The persistence of the investor share in new mortgages raises questions about the role of negative gearing, coinciding with falling rental yields amid increasing house prices. These discussions are expected to proliferate once the Federal Budget is released, particularly as policymakers tackle the growing imbalance in home ownership versus rental dominance.

Concluding Thoughts

The CGT discount’s introduction, combined with other significant elements like interest rate shifts and government incentives, has created a complex interplay influencing the trajectory of Australia’s housing market. If the goal is to enhance home ownership amongst Australians, a reevaluation of the current system is necessary, directing attention towards reducing the proportion of homes owned by investors.

As the government prepares to potentially amend these policies, the proposed changes may signal a pivotal shift aimed at improving housing accessibility for future generations.